Public ledgers revealed what was possible, but real-world finance requires shielded infrastructure with oversight where needed.

Blockchains promised to rebuild trust through transparency. But in practice, radical transparency created new problems. A system where anyone can observe balances, follow transaction flows, and build behavioral profiles is not what most businesses or individuals expect from a payment network. Privacy in financial systems has never been about cryptography alone, because it has always been about trust.

The real question is how to preserve confidentiality while maintaining the accountability that makes blockchain valuable.

Why Transparency Alone Doesn’t Create Trust

Transparency helps verification, but it does not automatically create trust.

The result is that many organizations either avoid blockchain infrastructure entirely or layer on costly privacy solutions that reintroduce the centralized intermediaries blockchain was meant to eliminate. This is one reason why regulated finance often requires added layers of complexity, off-chain agreements, or application-level workarounds to function on public chains.

Some systems reacted by pushing in the opposite direction: hiding everything. Fully opaque models can be technically impressive, but they raise another challenge. If activity cannot be assessed at all, then enforcing rules, detecting abuse, or satisfying compliance requirements becomes difficult.

The CEO of Binance, CZ, wrote the following on X:

“(Lack of) Privacy may [be] the missing link for crypto payments adoption.”

Privacy without accountability tends to remain isolated from institutions and regulated markets.

Consider a multinational corporation paying suppliers across jurisdictions. It needs to prove compliance with sanctions and tax rules without broadcasting negotiated pricing to competitors. Or a digital-native company paying contributors in 40 countries. Individual earnings must stay private, yet tax authorities need proof that withholdings were correct. Public ledgers expose too much. Fully private systems prove too little. Current workarounds add friction that undermines blockchain's advantages.

Concordium’s Direction: Privacy With Accountability

Concordium's development team focuses on making privacy structural rather than optional. The network supported shielded transactions back in 2024, but the implementation lacked features critical for regulatory compatibility. Protocol-Level Tokens had not yet been developed, and shielded transactions applied to CCD, a utility token, offered limited practical value. A consensus has been reached in 2026 that they would return to the Concordium blockchain, however, in a new, Smart Money supporting way.

With the growth of the stablecoin ecosystem, and increased network activity through various partnerships, shielded transactions and encrypted balances will become a natural fit as another characteristic of the next-gen privacy infrastructure.

Here is a proposed way of how they could work:

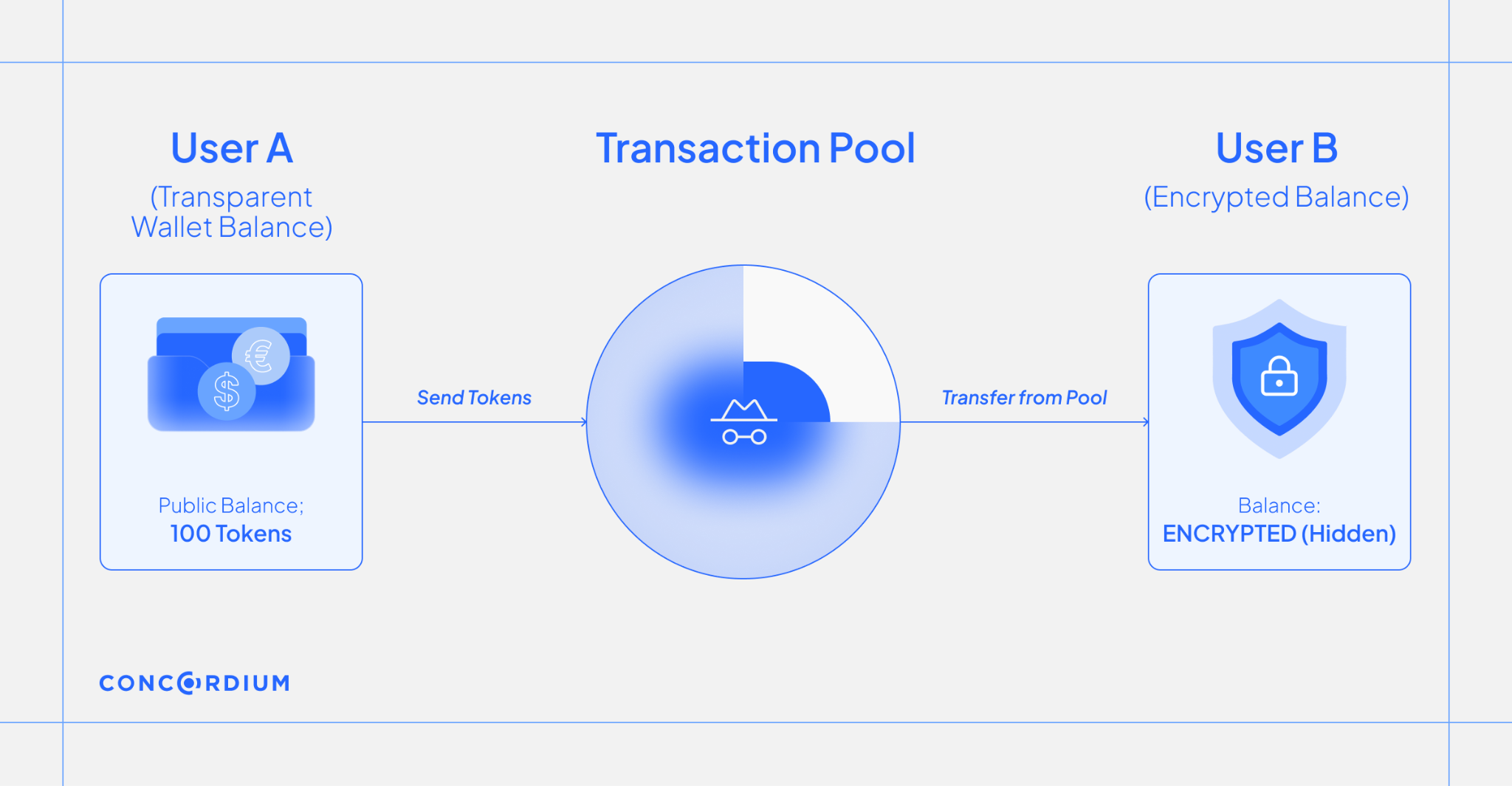

User A (transparent balance) can shield their transfer to User B (encrypted balance) → User A sends the tokens to a transaction pool, which makes the tokens mix with other assets. User B receives the tokens from the pool, but since the transaction and the balance are encrypted, this is not easily observable for a regular blockchain activity tracker.

This example is not just limited to two users, it can also be applied to merchants, exchanges, and any entity using wallets on the Concordium blockchain. An exchange may want to prove reserves or compliance without exposing every customer flow publicly.

Shielded transactions do not mean permanently opaque token transfers. This system includes viewing keys, cryptographic keys that can be shared selectively to allow a third party to decrypt transaction history.

The principle is the same: confidentiality by default, accountability by design.

Monitoring Without Public Surveillance

Trust in finance requires continuous monitoring, but monitoring does not need to mean public exposure. Independent professional actors such as chain-analysis providers can operate as Transaction Privacy Guardians, assessing risk and supporting compliance workflows without turning the ledger into a public surveillance system.

Multiple guardians can operate in parallel, avoiding concentration of power while maintaining institutional-grade oversight. Exchanges and regulators can rely on corroboration across independent providers, much like risk monitoring works today.

A Blockchain Built for Real-World Finance

The goal is not to replicate traditional finance, but to bring its proven trust properties into decentralized infrastructure. Privacy, accountability, and regulated usability are not contradictions, they are requirements for blockchains that want to support real-world payments at scale. What comes next is a ledger where confidentiality is default, oversight is continuous, and trust is enforced by design.

That infrastructure is what makes blockchain ready for finance as it actually works.

Join the Concordium Community, follow us on X.